Part 2 of BIG Media’s special report on rare-earth elements

Key takeaways

- Most of the global economic value in rare-earth elements (REEs) is captured in the midstream and downstream segments, where China controls nearly 90% of refining capacity and dominates high-purity oxide production. This remains the biggest bottleneck in global diversification efforts.

- China’s rare-earth dominance is the result of deliberate strategy – not geology alone. State-backed industrial policy, consolidation, cost advantages, and lower domestic prices enabled China to build a processing ecosystem the rest of the world struggles to replicate.

- Global trade flows are overwhelmingly concentrated in Asia, which accounted for ~90% of rare-earth compound trade value in 2023. China imported more rare-earth compounds than it exported in 2023, registering a $1.47-billion deficit.

- Myanmar (Burma) plays outsized strategic role, supplying more than 70% of China’s rare-earth compound imports. Political instability in Myanmar represents a single-point global supply chain risk.

- The U.S. remains deeply exposed to Asian supply chains, exporting and importing more than 80% of its rare-earth trade value through Asia, despite policy efforts to rebuild domestic production. China’s rare-earth trade volume is seven times larger than that of the United States.

Broadly, there are three stages required to produce rare-earth elements (REE) from their ores:

-

- Separation of a concentrate of REE-bearing minerals

- Cracking of the REE minerals to liberate the REE into an aqueous solution

- Separation of REEs into individual elements

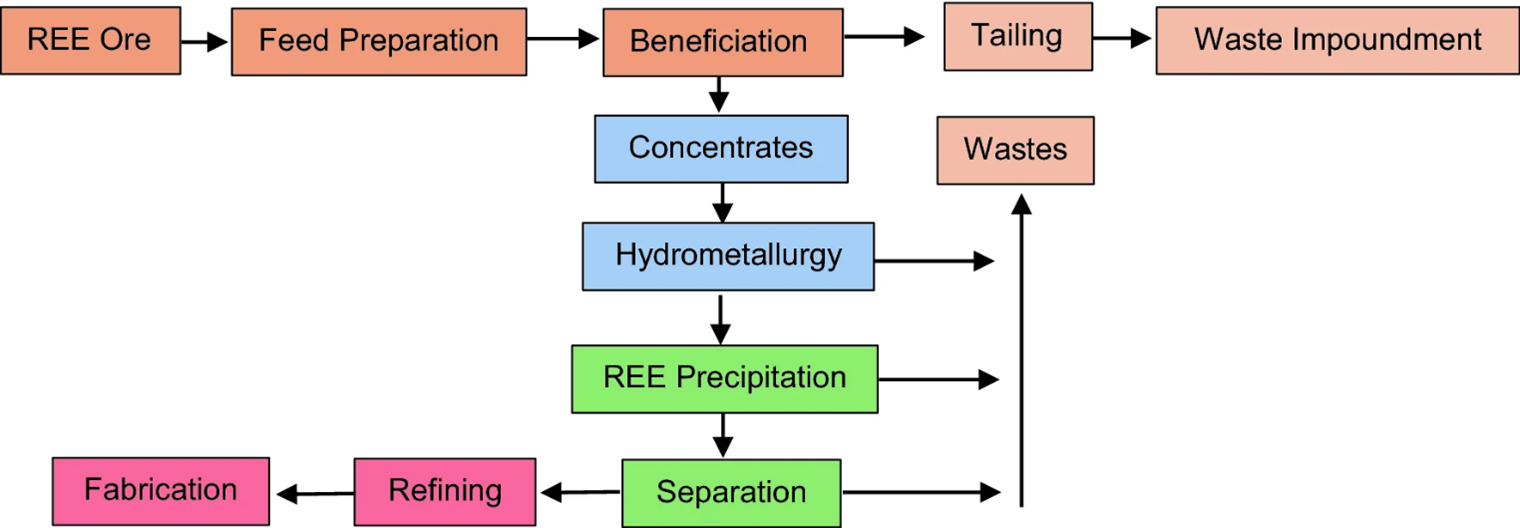

Separating rare-earth oxides (REOs) from mined ore involves a series of beneficiation and chemical processing steps. The ore is first crushed and ground, then concentrated and chemically leached, followed by solvent-extraction processes that isolate individual high-purity REOs for use in advanced manufacturing, energy technologies, and defence applications.

This process generates large volumes of waste (Figure 7) that can contaminate water sources and disrupt natural habitats if not properly managed. The combination of chemical residues, tailings, and – depending on the deposit – radioactive by-products introduces environmental and regulatory risks that operators must actively mitigate. The process is also highly energy intensive and often requires substantial labour input, factors that influence project economics, long-term operating costs, and licence-to-operate considerations.

Figure 7 – Schematic of the process by which REE ores are processed to metals, capturing the upstream, midstream, and downstream segments of the value chain.

The upstream stage as per Figure 7 runs from the mining for the REE ores and beneficiation to the production of concentrates made up of 40-70% REO, depending on the deposit type.

The midstream segment encompasses chemical refining, including leaching, impurity removal, solvent extraction, and controlled precipitation. These steps result in high-purity rare-earth oxides – typically at 99% purity or higher – which can be used in alloying and metal making. The midstream segment encompasses chemical refining, including leaching, impurity removal, solvent extraction, and controlled precipitation. The subsequent conversion of these oxides into metals through electrolysis or metallothermic reduction is a separate step that bridges midstream and downstream activities.

The manufacturing process (fabrication) is the downstream segment of the value chain in which rare-earth metals and compounds are transformed into high-value products such as catalysts, permanent magnets, specialty alloys and glass. This stage is where the bulk of the economic value is captured and is strategically important for technology supply chains.

The production of refined REEs is highly concentrated in China, which accounts for 87% of the world’s supply. The refining of REEs is in the midstream segment of the value REE supply chain as illustrated in Figure 7.

How China came to dominate global REE supply

In 2024, China’s share of global rare-earth mining was ~70% even as it accounts for ~90% of global processing. This outsized share of global supply and processing of rare earths has been achieved by an alignment of several factors.

China came to dominate rare-earth supply by a combination of:

-

- Its resource endowment

- Deliberate state-led industrial strategy

- Export controls

- Low production costs

- Downstream manufacturing capture

- Tight regulatory consolidation

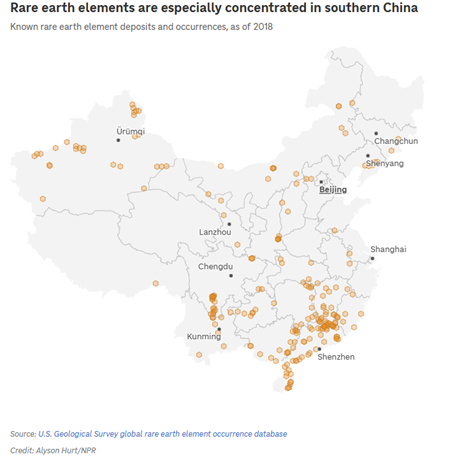

As noted, China possesses ~50% of global reserves of REEs. The Figure 8 map of China’s distribution of rare-earth elements shows concentration in the southern part of the country.

Figure 8 – Distribution of rare-earth element deposits in China shown to be mainly concentrated in southern China. Source: How China came to rule the world of rare earth elements

In addition to this resource endowment, China’s National Mineral Resources Plan (2016-2020) explicitly lists REEs as strategic minerals requiring state protection, planning, and security measures. Although this is a more recent policy document, it builds on and hardens the Chinese market position on REEs.

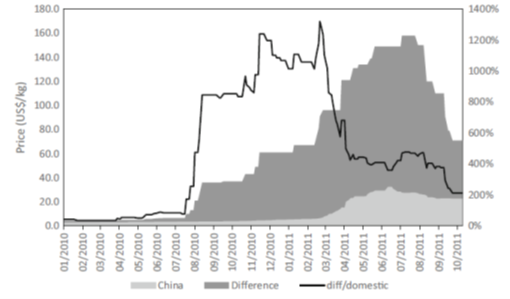

The price of REEs also played a role in expanding the size of the downstream sector in China. Domestic price of RE was significantly lower than the export prices, thus incentivizing the expansion of downstream domestic RE production.

Figure 9 – Comparison between the Chinese domestic rare-earth (cerium) prices and the export prices. Source: China’s public policies toward rare earths, 1975–2018

In Figure 9, the light-grey portion of the graph (bottom) represents the domestic price, while the dark portion represents the difference between the international price and the domestic price. The black line shows the differential as percentage of the Chinese domestic price.

The spread between domestic and international prices of rare earths could be as high as 1,200% of the domestic price, suggesting that international prices were up to 13 times higher than the domestic prices. This arbitrage in the prices served as an incentive in the buildout of the needed processing capacity domestically.

Following the money – rare-earth trade flows

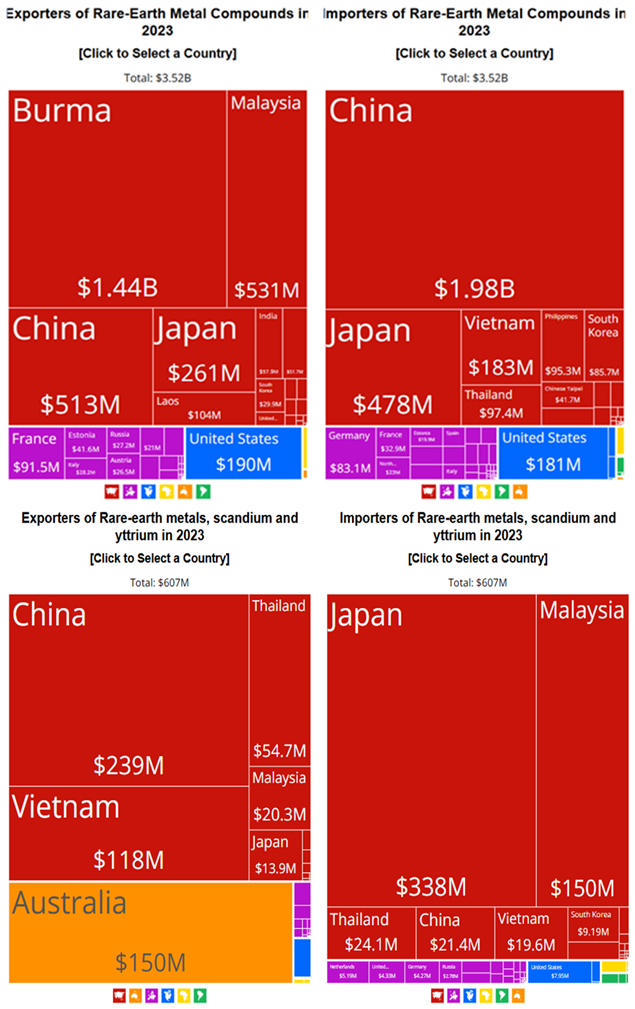

In 2023, total trade in rare-earth metals and their compounds was $4.127 billion, consisting of rare-earth metal compounds (HS 2846) of $3.52 billion and rare-earth metals (HS 280530) of $607 million. This compares to a total of $1.725 billion in 2018, made up of $1.27 billion in rare-earth compounds and $455 million for rare-earth metals. The value of trade in rare-earth metals was about 20% of the trade in rare-earth compounds in 2023, compared to 35% in 2018. Over the past five years, trade in the rare-earth metals (HS 280530) category has grown at an annualized rate of 5.93%, while trade in rare-earth-metal compounds (HS 2846) has grown at an annualized rate of 22.5%.

Focused on the rare-earth metal compounds in Figure 10, 86% of exports in 2023 were from Asia, led by Myanmar (Burma) at $1.44 billion, Malaysia at $0.531 billion, and China at $0.513 billion. Asia also led global imports – taking up 86% of global import. The top 3 importers of rare-earth metal compounds were China ($1.98 billion), Japan ($0.478 billion), and Vietnam ($0.183 billion). Chinese imports were largely drawn from Asia (93%), led by Myanmar, which exported $1.44 billion worth of rare-earth metal compounds to China.

Figure 10 – Value of export and import of rare-earth metal compounds and rare-earth metals by country in 2023. Asia dominates this trade. Visit Rare-Earth Metal Compounds for the interactive graphs. Source: Observatory of Economic Complexity

In the rare-earth metals category (Figure 10), Asia also dominated trade, accounting for 73% of the $607 million worth of global rare-earth metals export trade value in 2023. China led in the export of rare-earth metals, worth $239 million. Australia shows up notably with exports valued at $150 million.

On the import side of rare-earth metals, Asia leads in imports as well – importing $570 million worth, which was 94% of the import trade value. Japan’s import value of $338 million was 56% of the value of global value of imports. All of Australia’s exports of rare-earth metals were imported by Malaysia.

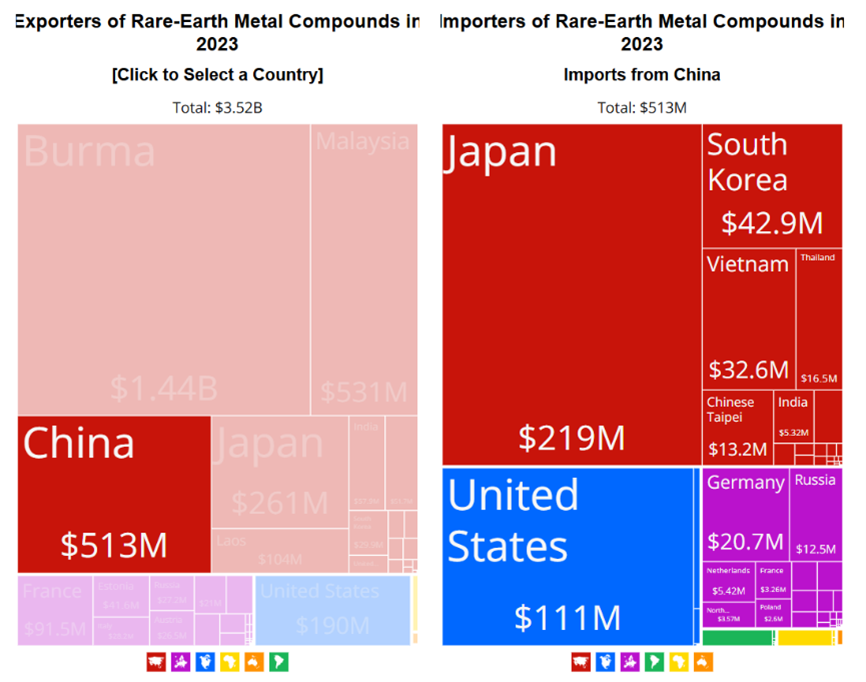

As seen in Figure 11, which is focused on the destination of Chinese exports of rare-earth metal compounds, the 67% of $513 million of 2023 exports were headed to Asia, dominated by Japan ($219 million), with South Korea a distant second ($42.9 million), then Vietnam ($32.6 million).

The United States’ import of rare-earth compounds was a total value of $181 million (Figure 10), of which $111 million was from China.

Figure 11 – Who imported China’s export of rare-earth metal compounds in 2023. Japan imported 40%+ of China’s $513-million export, nearly twice the U.S. import. Visit Rare-Earth Metal Compounds for the interactive graphs. Source: Observatory of Economic Complexity

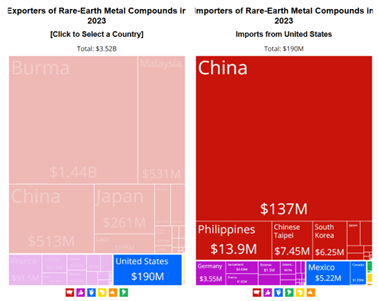

Note that Figure 12 shows the U.S. exported $190 million worth of rare-earth metal compounds in 2023, 89% of which went to Asia, led by China ($137 million) and followed well back by the Philippines ($13.9 million).

Figure 12 – Illustration of who imported the United States’ export of rare-earth metal compounds in 2023. China imported 70%+ of the U.S.’s $190 million in export, 10 times the Philippines’ import. Source: Observatory of Economic Complexity

The trade (measured in USD value) in rare-earth metal compounds is ~90% concentrated in Asia. On rare-earth metal compounds (global trade worth $3.52 billion, 2023), China ran a deficit of $1.467 billion. However, it ran a surplus of $217.6 million on rare-earth metals trade.

Overall, China is indeed a significant exporter of rare-earth metals and their compounds. It exported $752 million worth, of which $549 million was to Asian countries. More significantly, China also imported $2 billion worth of rare-earth metals and their compounds, of which $1.86 billion was from Asian countries. Globally, therefore China ran a total deficit of $1.248 billion on rare-earth metals and their compounds. With respect to the Asian region, China ran a deficit of $1.31 billion.

The United States’ trade in rare-earth metals and their compounds is significantly exposed to the Asia region. The total value of rare-earth metals and their compounds exported by the U.S. in 2023 was $193.64 million, 87% of which was to Asia. On the import side, the U.S. import of rare-earth metals and their compounds were valued at $188.95 million, 80% of which was from Asia. Overall, the U.S. maintained a small global trade surplus of $4.69 million.

Chinese trade in rare-earth metals and their compounds in 2023 was valued at $2.75 billion, seven times the US trade value of $0.38 billion. In 2018, China’s trade was valued at $0.711 billion, roughly three times the U.S. trade value of $0.24 billion at the time.

Conclusion

REEs have evolved into playing a major role in the modern economy and are set to play an even bigger role in the decades to come, with the projected increase in electricity generation from wind and solar, the electrification of transport, and expanded deployment of artificial intelligence infrastructure. Demand for REEs is expected to increase from 91 kilotonnes (2024) to 127 kt by 2035 (McKinsey) or 150 kt by 2040 (IEA). As a result of the key role REEs play – especially in defence, energy, and communication – they are classified as critical minerals for their economic impact and vulnerability to supply disruption.

Despite the term “rare” in the name, these elements are geologically abundant but “strategically scarce”. The challenge has never been sheer scarcity, but the political and economic will to build secure, ethical, and environmentally responsible supply chains. Their concentration in global supply chains is the result of economic incentives, permitting barriers, environmental constraints, and China’s long-term industrial strategy, not a lack of mineral abundance.

Much of the discourse on REEs is on the dominant position of China in the supply chain, and the geopolitical leverage it wields as it emplaced export controls. At the same time, China is not invulnerable. China itself is highly reliant on imports of rare-earth metal compounds. In 2023, China imported $2 billion worth of rare-earth metals and compounds, 70% of which was from a single country – Myanmar. This represents a critical vulnerability in its supply chain, making the political instability of Myanmar an immediate risk to the stability of global supply chains.

Nevertheless, Chinese dominance is expected to continue – the International Energy Agency – in its Global Critical Minerals Outlook, 2025 – projects that China will still control 75% of global rare-earth mining by 2040. The balance can shift, but it will take time, political will, capital, and the right regulatory environment. The supply required to meet increasing demand has been given by nature, but will policy choices complement the gift of geology? The answer will determine who holds leverage in the technologies that define the 21st century.

(Kaase Gbakon, BIG Media Ltd., 2025)